What Rising Fashion Brands Need to Understand About 2027

Why rising fashion brands should stop building collections and start building points of view. A look at what's actually selling heading into 2027, and what it means for founders.

Look at what's actually selling right now and you can see the future in pretty sharp relief.

The four best-selling fashion items on Who What Wear last year were all Adidas sneakers. Puma's Speedcat, a minimalist runner revived from the early 2000s, became the shoe Dua Lipa and Rihanna were photographed in, and every stylist in New York and London started recommending it. Silver metallic sneakers, ballet flats with running-shoe soles, and approach shoes built for rock scrambling are the three silhouettes trending into summer. On StockX, secondhand Nike and Ugg outpaced traditional sneaker growth. Louis Vuitton rose four positions year over year on the resale market, driven almost entirely by the Murakami collaboration, and Sprayground cracked the top five fastest-growing accessories brands.

McKinsey's State of Fashion 2026 report called jewelry the fastest-growing category in all of fashion, forecast to grow at more than four times the rate of clothing. Smart eyewear is heading for a breakout year, with multiple product launches scheduled as major players try to do what Google Glass couldn't. The second-hand market overall is tracking to grow two to three times faster than the first-hand market through 2027.

That is the shape of demand right now. It is not subtle. And it tells you almost everything a rising brand needs to know about where to place bets going into 2027.

Accessories are where attention is going

The quiet story underneath every trend report this year is that clothing has stopped being the center of gravity in fashion. Shoes, bags, jewelry, and eyewear are the categories compounding. McKinsey is explicit: jewelry alone is growing at four times the rate of apparel, driven by self-expression, self-gifting, and a broader consumer appetite for investment pieces that hold value.

For rising brands, this reframes the founder question. If you are launching in apparel, you are entering the hardest, slowest-growing, most saturated category in fashion, with the highest return rates and the lowest resale value per unit. If you are launching in accessories, you are entering the part of the category that customers are actually reaching for, that creators post about, and that holds up in the resale economy that now sits underneath every purchase decision.

This is not an argument against building an apparel brand. It is an argument for being honest about what you are building and where the growth actually is. The emerging brands getting traction right now understand this almost instinctively. Alfie, the Paris label behind the backless top Dua Lipa wore, built its early reputation on one reimagined silhouette rather than a full seasonal collection. Gluc Gator turned knitwear basics, including booty shorts, into the category people actually wanted from them. These brands did not try to be everything. They picked a specific product gesture and built a point of view around it.

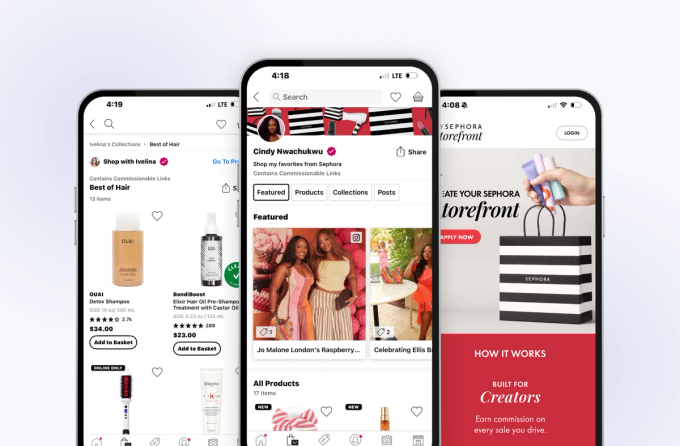

The Sephora and Gap move is the one to study

Both Sephora and Gap launched their own creator platforms this year, and the move deserves more attention than it has gotten. On the surface it looks like a reactive play, another scramble to catch Gen Z where they already are. Look closer and it's something more structural.

Sephora and Gap have figured out that Gen Z does not discover products through brand websites, brand ads, or brand email. They discover through creators, and they purchase through the nearest frictionless path, which is increasingly TikTok Shop. Global TikTok Shop GMV is tracking toward $50 billion by the end of this year. Two-thirds of first-time luxury buyers say their first brand exposure came through social media. The brands building their own creator platforms are not doing it for marketing reach. They are doing it because the creator layer is now the retail layer, and whoever owns the relationship with creators owns the funnel.

For rising fashion brands this reframes the whole go-to-market question. You are not building a brand with a creator strategy. You are building a brand whose product, pricing, and drops are deliberately designed as raw material for creators to remix. The drop cadence matters. The price points matter. The physical packaging matters, because unboxing is content. The styling guide matters, because creators need a visual vocabulary to riff on. These are product and brand decisions, not marketing decisions.

The AI question is a positioning question

Every rising brand is going to face a real choice about AI in its customer-facing creative, and the choice itself has become a brand statement.

Teddy Stratford has been open about using generative AI to produce ad imagery featuring its actual garments on virtual models in virtual locations, saving tens of thousands of dollars per campaign. Aerie recommitted to a no-AI pledge in 2025, committing to real models and ending all retouching, extending a position the brand has held since 2014. Both are legible, defensible positions. Both have customers who love them specifically for the stance they take.

The brands that lose are the ones that drift into AI use without a point of view, because their agency is cheaper that way, or because everyone else is doing it. That drift reads as characterless three years from now, when customers can tell the difference between a brand that chose AI and a brand that defaulted into it. Gen Z in particular has shown a well-documented ability to spot the gap between a brand's claims and its actual practice. Consumer researchers have started calling it a low tolerance for "trying too hard." A brand position on AI is not optional in 2027. The only question is whether you make it deliberately or inherit it by default.

Resale as a first-class product strategy

The secondhand numbers are no longer a trend. They are the market. Nike and Ugg posted faster growth in secondhand than in new sales on StockX last year. The Row built one of the most talked-about luxury brands of the decade with no advertising, no logo, and no social media, relying entirely on word of mouth and a resale market that treats its pieces like investment goods. Bottega Veneta introduced a lifetime guarantee on bags, which is a product decision, a sustainability decision, and a resale-value decision at the same time.

For rising brands this means resale has to be part of the product thinking from day one. If a piece does not hold value on Depop, Vestiaire, or Grailed, the brand is leaking equity every season. The materials, the construction, the labeling, the documentation, the limited runs, the drop scarcity, all of it feeds into whether your product has a second life and a third owner. Resale value is now a proxy for brand strength in a way it never was before.

Adjacent to this, the 2026 FIFA World Cup and the Milan Olympics are both expected to drive a surge in sport-linked fashion. StockX is forecasting soccer's influence on U.S. fashion to accelerate significantly, and artist-led sneaker collaborations, including a fully original signature Adidas from Bad Bunny, are lined up to anchor the season. For rising brands in streetwear, accessories, or anything adjacent to sport culture, these are once-per-cycle demand events that shape consumer attention for eighteen months. Missing them is not a minor tactical mistake. It is a product calendar issue that should be on every founder's planning wall right now.

The fundamentals have not changed, but the weights have

Brand strategy has always been about making deliberate choices in the face of infinite possibility. That has not changed. What has changed is which choices compound and which ones dissolve.

Choosing a category that is actually growing compounds. Launching with a single signature product instead of a full collection compounds. Building for the creator layer compounds. Designing for resale value compounds. Taking a clear position on AI compounds. Timing your drops around sport culture compounds.

Building a brand that looks and sounds like every other brand using the same tools and templates does not compound. It evaporates. The rising fashion brands that will matter in 2027 are the ones making specific, legible, defensible choices at the product level, and letting those choices ladder up into a brand story customers can repeat without looking at the label.

Gary Little is the Founder of Nufero, a brand strategy and creative agency working with consumer brands on positioning, identity, and go-to-market.